Business Continuity Test Tax

Business Continuity Plan Template Inspirational Express Bcp Business Continuity Plan Te In 2020 Business Continuity Planning Business Continuity Business Letter Format

Create A Business Continuity Plan In 4 Easy Steps Travelers Insurance Business Continuity Business Continuity Planning Risk Management Strategies

Business Continuity Planning Flevy Com Blog

How To Create An Effective Business Continuity Plan

Pdf Business Continuity Of Business Models Evaluating The Resilience Of Business Models For Contingencies

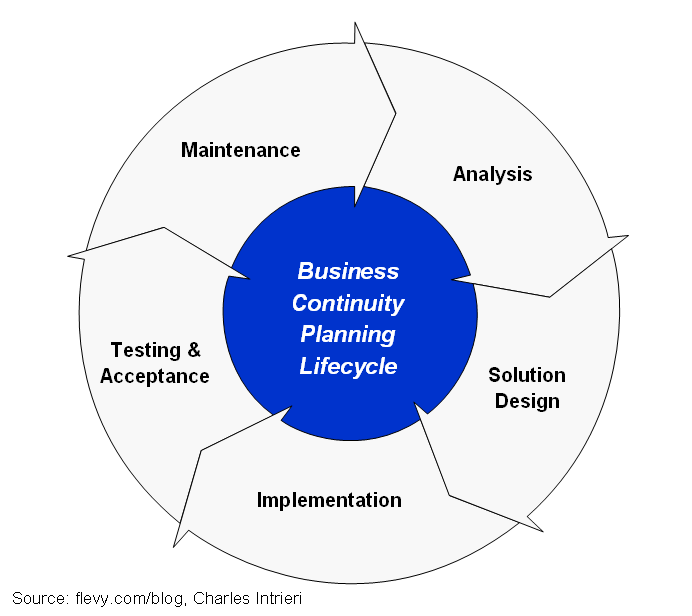

Business Continuity Planning Life Cycle Services Business Continuity Planning Business Continuity Business Infographic

The amendments are backdated to income years starting on or after 1 july 2015.

Business continuity test tax. Owners and directors of companies need to be aware of the conditions. Companies carrying forward tax losses from a prior year must satisfy the ato s continuity of ownership test cot or if unable to do so the same business test sbt for losses to be deductible against assessable income of future years. The benefits may include significant reductions in corporate tax payable.

A taxation principle applicable to corporate mergers and acquisitions. This assisted the tax office to demonstrate that the challenges arising from the actual crisis events as well as the testing exercises that occurred. The doctrine holds that in order to qualify as a tax free reorganization the.

Under this test a company will be able to utilise tax losses made from carrying on a business against income. The ato released draft law companion guideline lcg 2017 d6 on 21 july 2017. This provides guidance on the new similar business test currently proposed by treasury laws amendment 2017 enterprise incentives no.

The tax office has appropriate mechanisms to test and evaluate its administration of business continuity enabling it to continuously reassess the effectiveness of its policies and procedures. As with the same business test the business continuity test applies to the deductibility of tax losses capital losses bad debts. If your company has past tax losses that haven t been used as a tax deduction this tip is for you check the conditions under which a company s past losses may be claimed as tax deductions.

Payroll During Quarantine How Important It Is To Have A Business Continuity Plan For A Payroll Outsourcing Provider Bpion

A Methodology For Developing A Business Continuity Strategy In 2020 Business Continuity Continuity Business

Business Continuity Plan Checklist Template Free Printables Word Excel Business Continuity Planning Business Continuity How To Plan

4 Steps To Creating A Basic Businesses Disaster Recovery Plan Business Continuity Planning Business Continuity Writing A Business Plan

Identity Theft Incidents Highlight Importance Of Cybersecurity Business Continuity Planning Business Continuity Health Plan

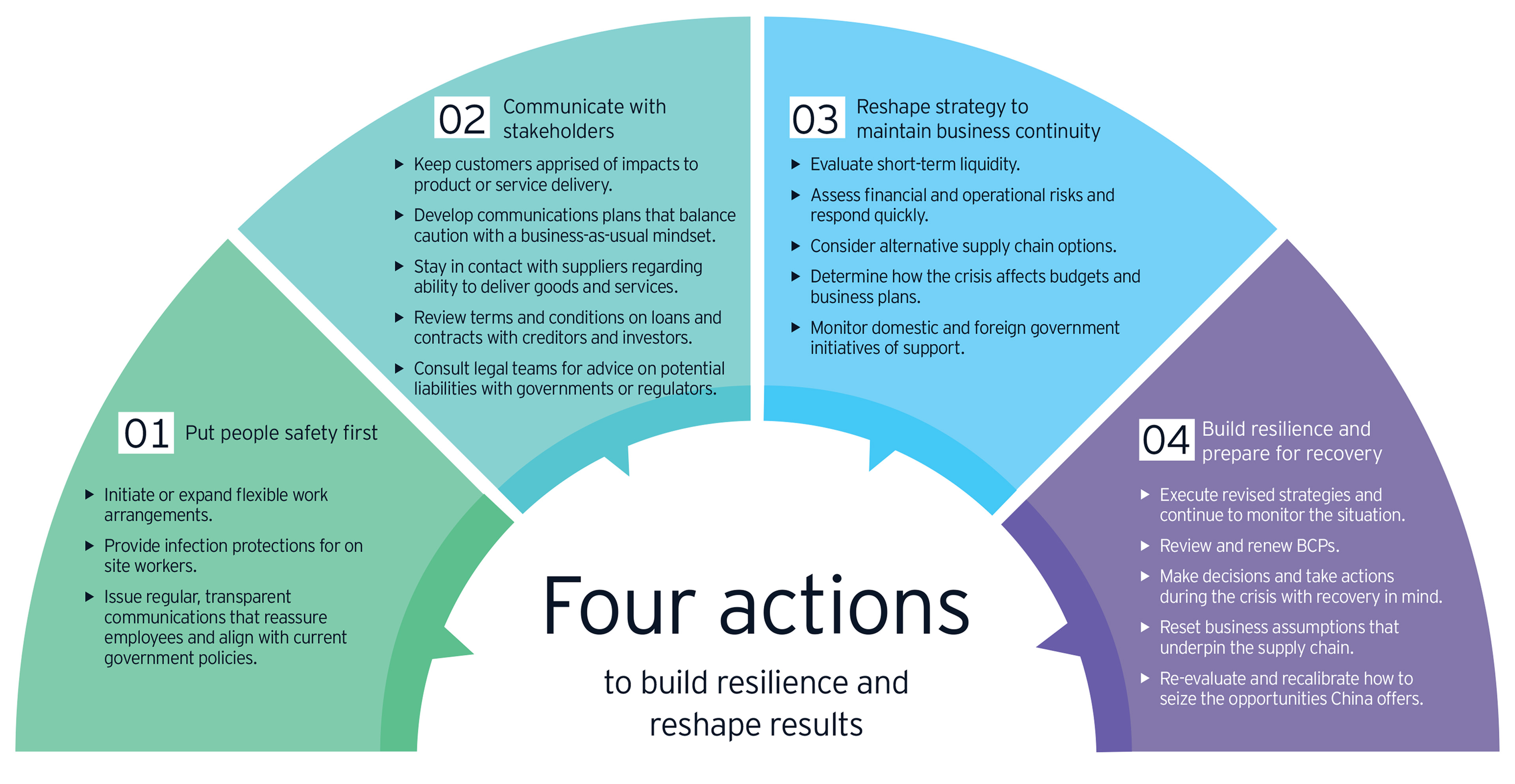

Covid 19 Business Continuity Plan Five Ways To Reshape Pagetitlesuffix

Business Continuity Plan Template New 7 Free Business Continuity Plan Templates Excel Pdf Formats In 2020 Business Continuity Planning Business Continuity How To Plan

Business Continuity Plan Management Template With Sle Business Continuity Templates Business Continuity Planning Business Continuity Business Contingency Plan

Example Image Business Continuity Planning Process Diagram Business Continuity Planning Business Continuity How To Plan

Disaster Recovery Business Continuation Business Continuity Planning Business Continuity Business Infographic

Infographic Cybercrime Costs On The Rise Infographicbee Com Business Continuity Planning Business Continuity Security Tips

Business Continuity Plan Template Putnam County Florida Chamber

Business Continuity Of Business Models Evaluating The Resilience Of Business Models For Contingencies Sciencedirect