Business Expenses Prior To Incorporation

Internal Control Audit Report Template 4 Templates Example Templates Example Audit Report Template Internal Control

Incremental Budgeting Meaning Advantages And Disadvantages Budgeting Accounting Finance Money Management

Amp Pinterest In Action In 2020 Agreement Business Template Sample

Incremental Budgeting Meaning Advantages And Disadvantages Budgeting Accounting Finance Money Management

Incorporation Expenses Double Entry Bookkeeping

Ieee Contract Large Agreement Negotiation Negotiation Skills

If i paid for my virtual car show company s startup expenses with my personal account before incorporation can i reimburse myself with funds from the corporate account and then deduct them in the first year.

Business expenses prior to incorporation. The credit entry sets up a liability representing the amount due by the business to the owner. Expenses incurred prior to a business being open for business are not expenses. These are termed as preliminary expenses or startup expenses.

They were under 5000usd. You can write off certain expenses as long as the business opens. Preliminary expenses could also be charged against capital reserve out of profit prior to incorporation.

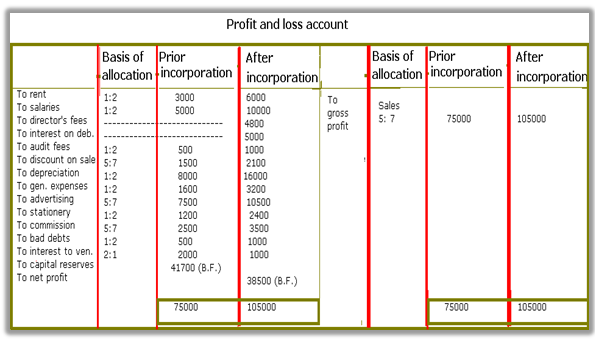

There is a separate category related to organizational costs fees associated with establishing the business like legal services. According to section 61 of the corporation tax act 2009 cta 2009 assuming any pre trading expenses are legitimate the expenses are treated as if they were incurred on the start date and therefore a deduction is allowed for them expenses can be claimed for up to 7 years before a company starts up in business. D expenses that are solely incurred for the company on and after its incorporation for example preliminary expenses or interest on debentures or directors fees should be charged wholly to the post incorporation period.

Credit the incorporation expenses have been paid by the owner from personal funds the business therefore owes this amount back to the owner. If your start up expenses exceed 5 000 you must depreciate any amounts above 5 000 over 15 years. Allowable expenses include those related to investigation such as travelling to potential business locations and preparation for example employee training.

This is from september to december. You would multiply the amortization period by 4 months. In the example 83 34 times 4 equals an amortization expense of 333 36.

Currently the small scale businesses and startup companies are unaware of the benefits that can be claimed regarding these expenses. The debit entry records the incorporation expenses which are the costs of setting up the business. 1 00 000 on condition that all profits earned from 1 1 2009 shall belong to the company.

Templates Joint Venture Agreement Templates Hunter Joint Venture Joint Agreement

Profit Prior Incorporation Accounting Education

Company Formation Services Rikvin Company Secretary Accounting Services Private Limited Company

Catering Agreement 4 Catering Contract Template Doc Easy To Download And Use Doc Business Templa Contract Template Business Template Business Plan Template

Contract For Catering Services Template Inspirational 13 Contract Templates Free Sample Example Format In 2020 Contract Template Free Brochure Template Template Free

Professional Services Contract Template Luxury 50 Professional Service Agreement Templates Contracts In 2020 Letter Template Word Contract Template Pamphlet Template

Corporate Financial Analyst Resume Sample 1 Financial Analyst Resume Sample If You Are The One That Searches For Financ Financial Analyst Analyst Financial

Artist Management Contract Template Beautiful 58 Management Agreement Examples And Samples In 2020 Contract Template Artist Management Management

Iras Tax Treatment Of Business Expenses A H

11 Attractive Event Photography Contract Template In 2020 Photography Contract Event Photography Contract Template

Gilead Sciences Initial Public Offering Prospectus January 1992 Www Slideshare Net Lucasbilling Initial Public Offering Science Executive Management

Section 35d Preliminary Expenses Untying The Knots

Pin On Professional Resume Template