Business Expenses Wholly And Exclusively

What Are Business Expenses What Expenses Can I Claim

Overseas Expenses Are Tax Deductible And You Can End Up Saving Hundreds Of Pounds In Taxes If You Have All The Ne Tax Deductions Deduction Accounting Services

Smeinfo Understanding Tax

Iras Tax Treatment Of Business Expenses A H

To Take A Refund On Tax While Keeping Or Purchasing Your Uniform Download Uniform Tax Rebate Form P87 Each Of An Employee Has To Fil In 2020 Tax Refund Tax Accounting

Money Saving Tips For Dentists Http Www Harleystreetaccountants Co Uk How Can Dentist Save Money Understanding Yourself Dentist Dental

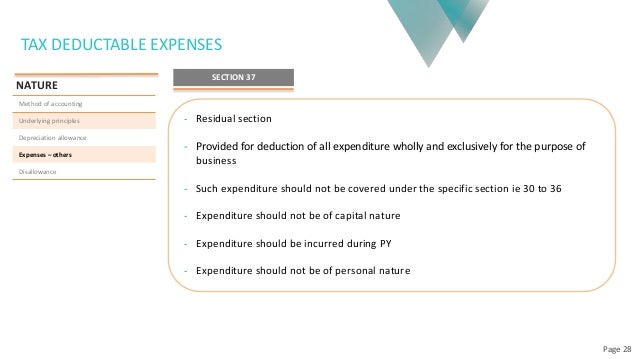

A business can only claim a tax deduction if the expenses are wholly and exclusively incurred in the production of income.

Business expenses wholly and exclusively. A deductible business expense. In what could set a precedent in the interpretation of wholly and exclusively allowable expenditure dr samad samadian has had his appeal dismissed by the hmrc tribunal the culmination of a seven year battle with them over his business mileage claims. The rule is that where an identifiable proportion e g.

It is often vary difficult if not impossible to. This means that the costs must be incurred while actually performing the business or trying to attract more business. Thirdly employer contributions are always paid gross and the employer can treat the contribution as a deductible business expense against their corporation tax bill for a trading year provided that the contribution is demonstrably in the ssas bank account before the company year end.

Wholly and exclusively the basic principles. How does this work for expenses which are partly for business purposes and partly for private purposes. The wholly and exclusively test can only be satisfied if the sole reason for incurring the expenditure is for the purposes of the trade in question.

Such an incidental benefit does not of itself. It goes a little something like this. When you are self employed you can claim a tax deduction for expenses which are wholly and exclusively for the business.

40 of the expense is wholly and exclusively for the business you may claim that proportion. All revenue trading expenses must have been incurred wholly and exclusively for the purposes of running the business to be allowable for tax purposes. Other legislation using the term wholly and exclusively the words wholly and exclusively also appear as part of the general expenses rule for employees in s336 income tax earnings and.

What business expenses are allowable. There are two matters for consideration in determining if this is the case one of law and one of fact. Where a taxpayer incurs an expense wholly and exclusively for the purposes of their trade profession or vocation an incidental benefit may arise.

Top 5 Free Online Courses With Certificates In 2019 Top Online Schools With Certificates Online Courses With Certificates Interview Preparation Coding

What Business Expenses Can You Write Off

Allowable Disallowable Expenses

Income Tax Malaysia General And Specific Deductions Docx Expense Tax Deduction

Contractor Expenses A Guide To Expenses And Claiming Boox

Business Expenses Classification Under Income Tax Sandeep Jhunjhunw

19 Ltd Companies Director S Expenses You Should Claim 2020

Detailed List Of Tax Allowable Expenses Raymond Benn Co Limited Chartered Certified Accountants Tunbridge Wells

Download This Photo In Liverpool United Kingdom By Jj Ying Jjying Black Cab London Black Cab About Uk

Dns Accountants Wembley Provides A Wide Range Of Accountancy Services Including Bookkeeping Payroll Accounting Accounting Services Chartered Accountant

8 Non Tax Deductible Expenses You Can T Claim In 2019 A Hmrc Guide

Vat Reclaim On The 45 Pence Mileage Allowance Fuel Element Family Guy

Foreign Business Travel Expenses And Allowances Explained