Business Expenses Under Income Tax Act

Smeinfo Understanding Tax

(viia).jpg)

Amounts Expressively Allowed As Deduction Under Section 30 To 37

Expenses Definition Types And Practical Examples

Iras Tax Treatment Of Business Expenses A H

Employee Expense Report Template 11 Free Docs Xlsx Pdf Report Template Business Template Report Writing Template

Expense Reimbursement Form Templates 17 Free Xlsx Docs Pdf Samples Templates Excel Templates Tutoring Flyer

General section 37 1 of income tax act.

Business expenses under income tax act. She is keen to understand how business expenses are allowed under the indian income tax act 1961. Disallowance of business expenditure on account of non deduction of tax on payment to resident payee sec. Generally only the cost of advertising in canadian newspapers magazines journals and on canadian television and radio networks can be deducted.

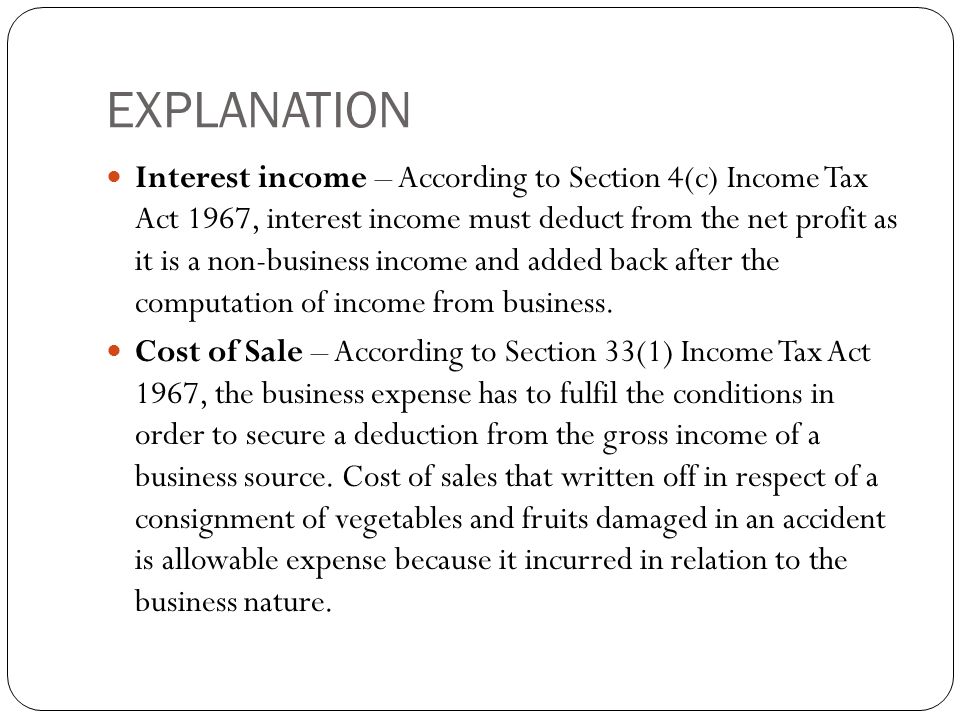

Year in which such tax has been paid. Any expenditure not being expenditure of the nature described in sections 30 to 36 and not being in the nature of capital expenditure or personal expenses of the assessee laid out or expended wholly and exclusively for the purposes of the business or profession shall be allowed in computing the income chargeable under the head profits. 40 a ia any interest commission or brokerage rent royalty fees for professional services fees.

What is an acceptable business promotion expense under the income tax act depends on what type of advertising you re doing and where you re doing it. As a knowledgeable person in taxation how will you address the worry of ms. Stock businessmen who trade stock of high value can claim such a deduction on the insurance premium.

However assessee engaged in a business and declaring income under presumptive tax scheme under section 44ad whose total sales turnover or gross receipts does not exceed rs 2 crore are not liable to get their accounts audited under section 44ab. Expenses covered under section 30 to 36. Cit supra case that the wealth tax on assets held by the assessee for the purpose of his business was deductible as a business expense in computing the assessee s income from business.

Insurance premium paid towards stock cattle and health of employees. If the gross turnover or gross receipts of business exceeds rs. If any expense is covered under section 30 to section 36 of the income tax act 1961 and could not be allowed due to non satisfying condition laid down under section same cannot be allowed under this residuary section.

As per the amendment brought by section 284 of the income tax amendment act 1972 any sum paid as wealth tax for the assessment year 1957 58 or any. The following expenses are allowed as deductions under section 36 of the income tax act 1961.

Problem Based Learning Project Tax Computation On Malaysian Food Service Mfs Sdn Bhd Group B Namematrik No Izwani Bt Abdul Majid Hazwani Bt Ghazali Ppt Download

Create A Comprehensive Profit And Loss Statement For Your Company With This Accessibl Profit And Loss Statement Statement Template Personal Financial Statement

Expense Reimbursement Form Template Beautiful Ms Excel Expense Claim Form Template In 2020 Templates Excel Templates Microsoft Word Templates

What Do I Need To Keep Track Of Small Business Expenses Google Search Small Business Accounting Business Expense Business Tax

Daycare Business Income And Expense Sheet To File Your Daycare Business Taxes Page 1 Taxtime Income Tax Tips Starting A Daycare Daycare Forms Daycare Contract

How To Handle Food And Meals Expenses For 2018 In 2020 Small Business Expenses Food Small Business Tax

03x Table 04 Income Statement Statement Template Financial Ratio

Unique How To Make Daily Expenses Sheet In Excel Xlstemplate Xlssample Xls Xlsdata Hilario

10 Steps To Launch A Part Time Business While Keeping Your Full Time Job Infographic Marketing Internet Marketing Company Infographic

Business Ownership Structure Types Business Structure Business Ownership Bookkeeping Business

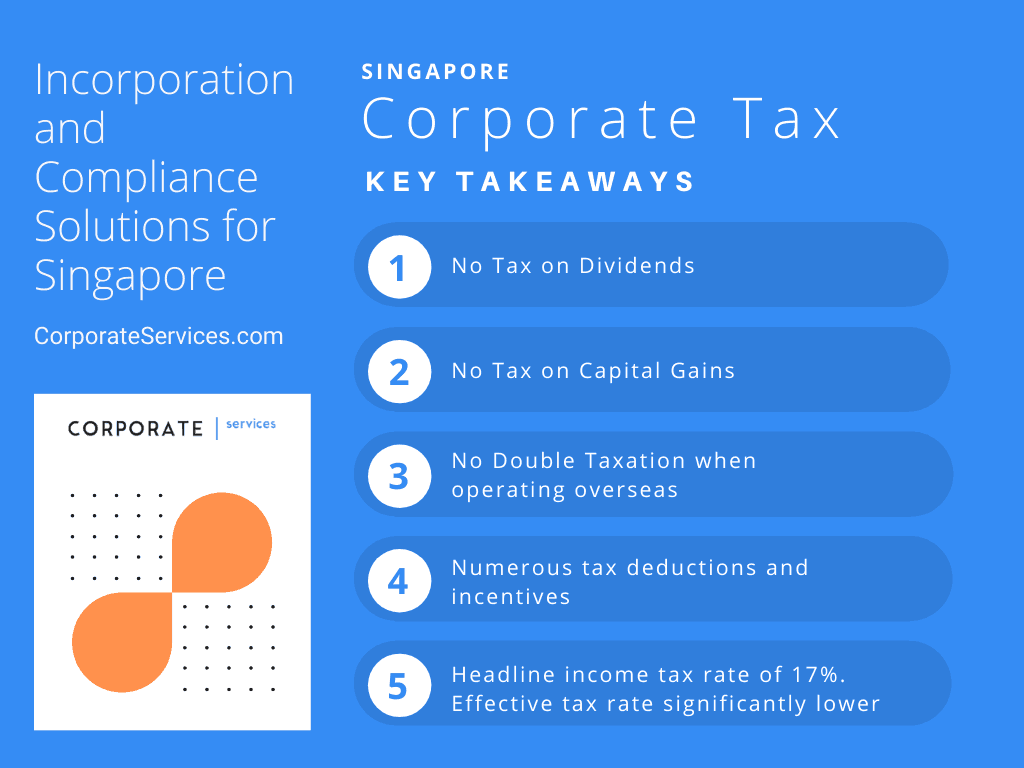

Singapore Corporate Tax 2020 Guide Taxable Income Tax Rates Incentives

Pin By Residential Landlords Association On Tax Income Tax Being A Landlord Budgeting

Expenses A Trader Can Claim In Itr Learn By Quicko